St. Patrick’s Day was last month, The Masters golf tournament was just a week ago, fiscal stimulus is hitting record numbers, and there’s a lot of talk of a Green New Deal. I love a four-leafed clover and I always get excited about The Masters, but I’m not sure about all this other “green” that is being talked about.

Last quarter a $1.9 trillion stimulus (“green”), known as the American Rescue Plan Act, was passed by Congress to pump more money into the US economy to help address the lingering effects of the Covid-19 pandemic. And, now President Biden is talking about a $2 trillion infrastructure bill.

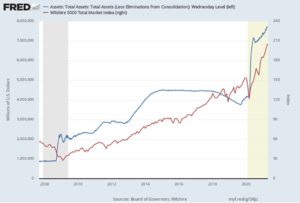

Here’s a chart to see the unprecedented amount of money being printed and put into circulation. This chart shows the Fed’s large-scale asset purchases from (09/03/2007 – 04/13/2021):

Yikes! With the continued printing of money, inflation has to be close behind, right? Right? Well, I think it depends on which side of the fence you sit. Do you believe in conventional economics? For those keeping score, I do. Or, do you believe in Modern Monetary Theory or MMT? MMT is a very “interesting” theory. If you don’t want to take the time to read the entire article about MMT, here is a brief description. Proponents of MMT believe that governments can simply print money to create wealth and jobs without any real consequences. Governments can also simply raise taxes or spend less without consequences. Interesting, right?

Would there ever be another bear market with this kind of thought process? Can we really print money and have a “free lunch”? Can we just raise taxes and cut spending whenever? Do we ever have to worry about a balanced budget? Of course, you and I do personally, but maybe some of our current government economists think they’ve got it all figured out… they’ll never have to balance a budget and inflation is nowhere to be seen.

Call me conventional, but debt matters, inflation is real, economies are cyclical, and markets have drawdowns. Whether MMT is being used or still a theory, that is yet to be seen. I like to be prepared for the worst and always hope for the best.

Speaking for preparing for the worst and hoping for the best, now for some thoughts on the market – Is the market expensive? Yes, but does it matter? Thanks to the Fed’s “large-scale asset purchases,” being expensive may not matter for today. We all know there is no free lunch, so, at some point, being expensive will matter—it always has. Here’s another axiom: “Don’t fight the Fed.” And that saying has been strengthened by the Fed’s new tool of asset purchases, also known as Quantitative Easing (QE). QE is a Fed tool that began with the financial crisis of 2008. Given its newness, we don’t know the long-term effects it will have on the financial markets. For now, we expect QE to be supportive to market prices.

“Supportive” doesn’t mean low volatility. We do expect an uptick in volatility this year. However, I believe it will be difficult for the S&P 500 to drop much beyond correction levels (did I just jinx it?). A correction is a drop in 10% or more. Rotations in leadership and contained general market pullbacks is what I believe volatility will look like for the next few months. Though, things can change and if they do, we aim to be prepared.

Circling back to the market being expensive – we have an updated chart of the Buffet Indicator. The Buffet Indicator is a ratio of total US stock market valuation to GDP. Warren Buffet uses this indicator as a market valuation tool, and, as you can see, it’s at its highest historical level.

So when does the bill come due? Are we robbing future generations of returns? Mortgaging our future? Does this printing of money and inflation really matter? In the words of my former UGA Economics professor, “It (inflation) matters when we say it matters, but, right now, we aren’t really talking about it.” This newly charted path is uncertain. Uncertainties in anything are always unsettling. That’s why we use a time tested quantitative risk approach that is designed to help us successfully navigate bull and bear markets and steward your portfolio on the best path no matter what lays ahead.

Please don’t hesitate to call or email if anything has changed. I’d love to hear from you.

You will find our most recently filed Form ADV Part 2 “Brochure,” including the Summary of Material Changes, at the following link: Trademark ADV Link

This Brochure, as well as additional information about our firm, is available on the SEC’s website, www.adviserinfo.sec.gov.

This material is intended for informational purposes only and should not be construed as legal, accounting, tax, investment, or other professional advice. Trademark Capital’s investment strategies are built using quantitative, proprietary algorithms that are designed to identify and react to changing market conditions. However, investors should be aware that no investment strategy or risk management technique can guarantee returns or eliminate risk in any given market environment. As with all investments, Trademark Capital Management’s investment strategies are subject to risk and may lose money. The investment strategies presented are not appropriate for every investor and individual clients should review with their financial advisors the terms and conditions and risk involved with specific products or services. Due to our active risk management, our managed portfolios may underperform during bull markets. Past performance is no guarantee of future results.