Inflation isn’t transitory. According to February’s US Consumer Price Index, inflation came in at 7.9% for the last 12 months, which is the highest year-over-year increase since April 1981. Needless to say, the Fed has a very tough job ahead to curb inflation.

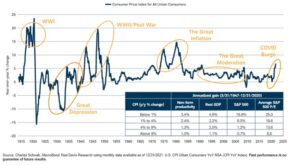

We all feel the inflationary pinch in our daily lives. We feel it whether that is filling up your car or going to the grocery store. Inflation also affects corporate profits and that matters to your retirement. Let’s revisit this graph from my last quarterly update to show the historical evidence of how inflation affects our markets and economy.

Why do corporate profits matter? Skeptics might say that corporate profits don’t matter much anymore with the way the market has continued to grow despite historically high valuations. As you can see in the above chart, inflation has always been a market disruptor. Will this time be different? Can the Fed engineer a soft landing?

Let’s look at a few ways inflation will affect corporate profitability and, in turn, your wallet and your retirement. Corporations have the following options:

- They can eat the higher costs, cutting into their own profitability.

- They can squeeze their suppliers, impacting the profit margins of the supplier companies.

- They can pass on higher costs to their customers, depressing demand and market share.

None of the above options are ideal for the companies or for you as an individual. Cutting into profitability will cut into valuations. How will this affect the historically high valuations? Will the growth stocks that have driven market uptrend continue their ascent? Or, do investors turn to Blue Chip value stocks during this phase of the market? In the past, Blue Chip stocks have been the preferred choice to weather market storms. Some were calling for this type of investing years ago while growth stocks continued upward. Why does this matter today? Well, if an investor is happy to purchase a stock with a P/E ratio of 30, the implication is that the next 30 years’ worth of earnings is adequate compensation for the cash price today. But the problem with a high inflationary environment is the far-off earnings decades from now should be discounted or penalized by a higher rate to accommodate for the corrosive impact of inflation. The valuation of a stock today should be less if its future earnings will not be worth as much in real terms. Just like a 30-year bond is more susceptible to inflation than a 10-year bond, a stock with a P/E of 30 is more sensitive to inflation than a stock with a P/E of 10. Makes sense, right?

With profitability cut and valuations in question, how exactly does inflation affect demand? The beauty of a free market economic system is that it contains self-correcting mechanisms that reign in excesses. Suppliers respond to high prices by producing more. Consumers respond to high prices by curtailing their demand or finding substitutes. Barring outside interference, the “invisible hand” will naturally guide supply, demand, and prices until an equilibrium is reached. However, that doesn’t mean that when these corrections occur, there won’t be losers. If the big post-COVID-19 run-up in the markets was driven by fiscal and monetary stimulus coupled with pent-up demand, it seems reasonable to ask how the market will fare once those market drivers are halted or reversed.

- Will higher airfare, rental car, and hotel prices cause vacations to be postponed?

- Will the surge in lumber and building supply costs cause homeowners to delay putting a new addition on the house?

- How expensive is it to hire labor to build that planned new addition?

- Will price spikes in staples like food and gasoline leave less money to be spent on fun items like a new flat-screen television or a new iPhone?

Every household has started to ask these kinds of questions. While each one of these decisions might not seem like much, together they make up two-thirds of the economy that is consumer demand. If inflation rises far and fast enough, it might dampen demand to the point of having a negative impact on the economy and the stock markets.

One of our favorite ways to measure the breadth between the number of stocks advancing versus the number of stocks declining is the McClellan Summation Index (pictured below). If the Index is above zero, we consider it positive. If the Index is below zero, we consider it negative. For a more in-depth explanation click here. The better the ratio of stocks advancing over declining, the healthier the market is. When the Index is negative and makes a strong move toward zero but fails and reverses direction as you see in the chart below indicated with the blue circle, this is not a good sign. There’s a good chance that the market low will be tested and decline to lower levels.

Again, we pose the question, “Can the Fed engineer a soft landing?” Currently no one truly knows and only time will tell. As we all know, inflation leads to uncertainty for markets. Uncertainty can be scary. As Vannevar Bush, a well-known policymaker during WWII, once said, “Fear cannot be banished, but it can be calm and without panic; it can be mitigated by reason and evaluation.”

Don’t give into fear and panic! Know that we are evaluating the markets constantly and aim to make changes to our strategies to help weather any upcoming storms. Please don’t hesitate to reach out with any questions you may have. We would love to hear from you.

Best,

The Trademark Capital® Team

This material is intended for informational purposes only and should not be construed as legal, accounting, tax, investment, or other professional advice. Trademark Capital’s investment strategies are built using quantitative, proprietary algorithms that are designed to identify and react to changing market conditions. However, investors should be aware that no investment strategy or risk management technique can guarantee returns or eliminate risk in any given market environment. As with all investments, Trademark Capital Management’s investment strategies are subject to risk and may lose money. The investment strategies presented are not appropriate for every investor and individual clients should review with their financial advisors the terms and conditions and risk involved with specific products or services. Due to our active risk management, our managed portfolios may underperform during bull markets. Past performance is no guarantee of future results.